As you must already know, a life insurance policy is a long commitment - it literally spans decades and, you need to put in your hard-earned money to pay the premiums. It is important to know how much you will be paying over this period and how it is calculated since the premiums depend on a number of factors. Premium rates differ from insurer to insurer and also vary according to your health, age, and lifestyle choices.

Let’s have a detailed look at the various factors that impact how much your life insurance costs!

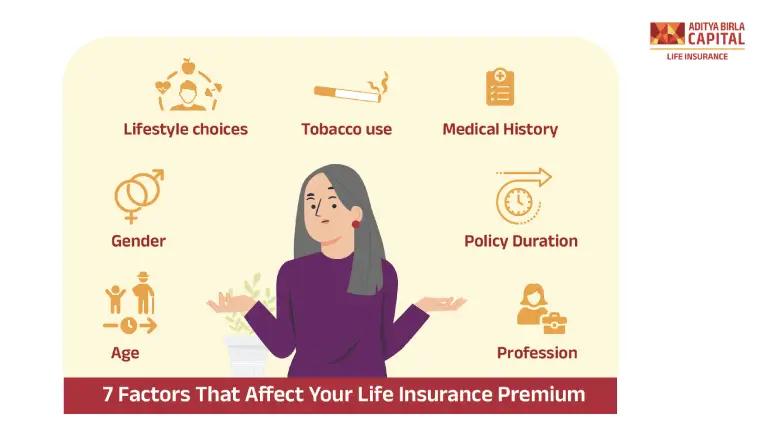

7 Important Factors That Affect Your Life Insurance Premiums

-

Age

The chief factor that affects the life insurance premium rate is your age. Younger people are healthier and less risky for the insurance company to cover since the probability of claims will be lesser. As you grow older, you become more susceptible to medical conditions. Even commonly prevalent diseases like diabetes, asthma, etc. can have a huge impact on your premiums. So, you should ideally buy life insurance when you are young.

-

Gender

The next important factor is your gender. Women, on average, tend to live longer than men and hence, insurers charge them lower premiums. A report by the 2022 Economic Surveys says that women have a longer expectancy rate as compared to men. So, it can be inferred that a woman might end up paying premiums for a longer time than a man, leading to lower premiums.

-

Lifestyle choices

Your lifestyle plays a big role in how much you pay for life insurance. Lifestyle means how you spend your time and what you like to do, including your health choices, hobbies, and interests. These choices can affect how long you live. For example, if you enjoy risky activities like kayaking, surfing, etc, your life insurance premiums could likely be higher. This is because such hobbies can be dangerous, and insurance companies might see them as risky.

-

Tobacco Use

"Smoking is injurious to health" is a health advisory that you can often see on screens during ads, movies, and series. It is true, smoking is really bad for you. But did you know it can also impact how much you pay for life insurance? Using any form of tobacco is harmful, no matter how little you use. Insurance companies know that smoking and other tobacco use can lead to serious health problems over time. This is why they ask questions about tobacco use when you apply for insurance to understand the risks you might bring. Questions might include: Are you a smoker? How many cigarettes do you smoke per day? When did you last use tobacco? And based on your answers, they will decide your premium. In essence, smokers typically pay more than non-smokers.

-

Medical History

Any insurance company will require you to go through a medical screening before signing up for the policy. This test helps them in evaluating your profile for any existing or future medical risks. Medical conditions can be hereditary or an outcome of your lifestyle. If you are diagnosed with a pre-existing severe medical condition while buying the policy, then your premium rates will be higher than that of a healthy person - since you will be a risky individual to cover.

For example, Anisha and Amina apply for term insurance plans. Anisha has diabetes, whereas Amina doesn’t have any pre-existing conditions. So, the premiums of Anisha’s policy will be higher

-

Policy Duration

The policy tenure also has an influence on the premiums you pay. The longer the duration, the longer the premium payment term. Short-term policies are cheaper than long-term policies

-

Profession

Your profession also plays a key role in determining the cost of your life insurance. If you are working in hazardous environments that can have an effect on your health, it can increase your premium. Industries like mining, fisheries, chemical, oil and gas have been known to have adverse health effects. This is why insurers might calculate higher premiums if you work in these professions

What Is the Age Limit for Life Insurance?

Life insurance policies usually require a minimum age of 18 years. The maximum age limit typically falls between 60 and 65 years, depending on the specific policy. It is also worth noting that some insurers may provide coverage to individuals beyond this age range as well

How Does Gender Affect Life Insurance Premiums?

Gender plays an important role in your life insurance premiums. Based on statistics, women tend to live longer than men - a fact supported by data. For instance, according to a 2022 report by MOSPI[2], the life expectancy at age 60 for males in our country is 17.5 years, whereas for females, it is 19 years.

The insurer considers various factors that could influence the likelihood of paying out the claim amount, known as the sum assured, which includes gender. Men typically have a shorter average life expectancy, which makes them a higher risk for insurers. Consequently, men are usually charged higher premiums compared to females.

What's the Best Age To Get Life Insurance?

Deciding when to get life insurance does not solely rely on age. You can choose the plan depending on your financial goals –

- For safeguarding your dependents, buying term insurance is crucial.

- For wealth creation, you can start young with a Unit Linked Insurance Plan.

- For specific goals like buying a house, vehicle, etc. opt for an endowment plan.

In essence, you should align your life insurance purchase with your financial objectives rather than age

Wrapping up!

We hope this article helped you understand the various factors affecting life insurance premiums. You can pay lesser premiums by taking into account the factors you can control, like buying insurance when you are young, maintaining a healthy lifestyle, etc. We recommend that you compare and weigh the different options available to choose the best policy for yourself

Table of Contents

Table of Contents