- All Insurance

- Endowment Plans

- Savings Plans

- Term InsuranceNew

- Retirement Plans

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Her Insurance

- Manage My Policy

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

Can You Buy a Life Insurance Policy Without a Medical Exam?

Get immediate income payout after 1 day of policy issuance^

Plan Smarter, Live Better!

Table of Contents

Table of Contents

How Much Helpful You Found This Article?

Rated by 0 reader

/ 5 ( reviews )

Not helpful

Somewhat helpfull

Helpful

Good

Best

Thank you for your feeback

FAQs on Insurance Companies Classify Smokers

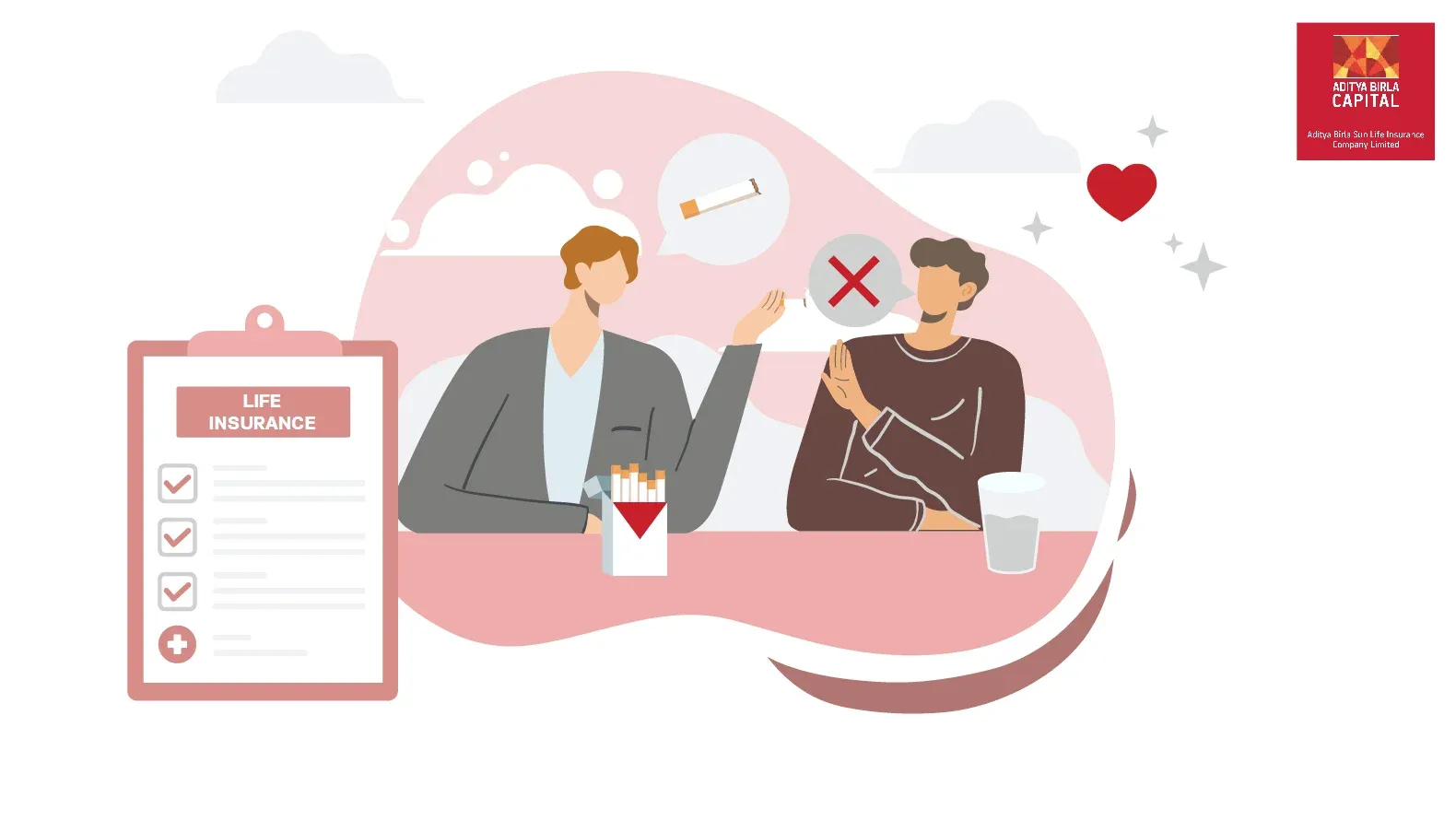

Insurance companies may require you to undergo a medical examination, which includes tests for nicotine and cotinine in your blood, urine, or saliva. These tests can detect if you have used tobacco or nicotine products within the last 12 months.

Smoker policies generally have higher premiums due to the increased health risks associated with smoking. They may also offer limited coverage and exclude certain smoking-related conditions. Nonsmoker policies, on the other hand, have lower premiums and more comprehensive coverage.

While being a smoker may not result in outright denial of life insurance, it can lead to higher premiums and limited coverage. Insurers may also impose waiting periods for specific smoking-related conditions or exclude them from coverage altogether.

Yes, quitting smoking can significantly improve your insurance rates. Most insurance companies reclassify policyholders as nonsmokers after they have been tobacco-free for a specific period, usually 12 months. Once reclassified, you may be eligible for lower premiums and more comprehensive coverage.

Yes, most insurance companies in India classify e-cigarette users as smokers since e-cigarettes contain nicotine. Consequently, e-cigarette users are likely to face higher premiums and limited coverage, similar to traditional tobacco users.

If it is discovered that you misrepresented your smoking status, your insurance policy could be cancelled, or your death benefits may be denied to your beneficiaries. It is essential to be truthful when applying for insurance.

Similar to life insurance rates smoker vs nonsmoker, health insurance premiums for smokers are higher than those for nonsmokers. Insurers may also impose waiting periods for specific smoking-related conditions or exclude them from coverage altogether.

Yes, occasional smokers who have smoked even just a few times within the last 12 months are generally classified as smokers by insurance companies, resulting in higher premiums and limited coverage.

To lower your insurance premiums, consider quitting smoking, shopping around for better rates, opting for group insurance, choosing a policy with limited coverage, and maintaining a healthy lifestyle.

Most insurance companies require you to be tobacco-free for at least 12 months to be classified as a nonsmoker, making you eligible for lower premiums and more comprehensive coverage. However, the specific duration may vary between providers, so it is essential to verify this information with your insurer.

Show All

Hide

Buy ₹ 1 Cr Term Cover

@Rs.575/month

for Salaried Individuals¹

ABSLI Salaried Term Plan

Exclusively For Salaried Individuals

4 Plan Options

Life Cover upto 70 years

Optional Accelerated Critical Illness benefit

Inbuilt Terminal Illness Benefit

Life Cover

₹1 crore

Premium:

₹492/month¹

Recently Added Article

Most Popular Calculator

ABSLI Salaried Term Plan (UIN:109N141V01) is a non-linked non-participating individual pure risk premium life insurance plan; upon Policyholder’s selection of Plan Option 2 (Life Cover with ROP) this product shall be a non-linked non-participating individual savings life insurance plan. Tax benefits are subject to changes in tax laws. Kindly consult your financial advisor for more details. #Provided all due premiums are paid. 1LI Age 21, Male, Non Smoker, Option 1: Life Cover, PPT: Regular Pay, SA: ₹ 1 Cr., PT: 10 years, Premium paying term: 10 years, Annual Premium: ₹ 5900/- ( which is ₹ 491.66/month) Premium exclusive of GST. On death, 1 Cr SA is paid and the policy terminates. ADV/10/23-24/2489